VAMA: A New Adaptive Moving Average

Reference:

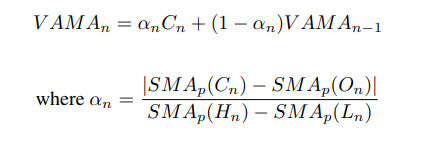

Definition

- The separation of the trend from random fluctuations (noise) is a major objective in technical analysis

- the simple moving average and the exponential moving average are the two most used filters used to achieve this goal

- those two filters use one parameter to control this degree of separation, higher degree of separation involve smoother results but also more lag.

- Lag is defined as the effect of a moving average to show past trends instead of new ones, this effect his unavoidable with causal filters and is a major drawback in decision timing .

- a new adaptive moving average technical indicator (VAMA) aims to provide smooth results as well as providing fast decision timing.

Calculation

Load basic packages

import pandas as pd

import numpy as np

import os

import gc

import copy

from pathlib import Path

from datetime import datetime, timedelta, time, date

#this package is to download equity price data from yahoo finance

#the source code of this package can be found here: https://github.com/ranaroussi/yfinance/blob/main

import yfinance as yf

pd.options.display.max_rows = 100

pd.options.display.max_columns = 100

import warnings

warnings.filterwarnings("ignore")

import pytorch_lightning as pl

random_seed=1234

pl.seed_everything(random_seed)

Global seed set to 1234

1234

#S&P 500 (^GSPC), Dow Jones Industrial Average (^DJI), NASDAQ Composite (^IXIC)

#Russell 2000 (^RUT), Crude Oil Nov 21 (CL=F), Gold Dec 21 (GC=F)

#Treasury Yield 10 Years (^TNX)

#benchmark_tickers = ['^GSPC', '^DJI', '^IXIC', '^RUT', 'CL=F', 'GC=F', '^TNX']

benchmark_tickers = ['^GSPC']

tickers = benchmark_tickers + ['GSK', 'NVO', 'AROC', 'GKOS']

#https://github.com/ranaroussi/yfinance/blob/main/yfinance/base.py

# def history(self, period="1mo", interval="1d",

# start=None, end=None, prepost=False, actions=True,

# auto_adjust=True, back_adjust=False,

# proxy=None, rounding=False, tz=None, timeout=None, **kwargs):

dfs = {}

for ticker in tickers:

cur_data = yf.Ticker(ticker)

hist = cur_data.history(period="max", start='2000-01-01')

print(datetime.now(), ticker, hist.shape, hist.index.min(), hist.index.max())

dfs[ticker] = hist

2022-09-09 19:39:16.539924 ^GSPC (5709, 7) 1999-12-31 00:00:00 2022-09-08 00:00:00

2022-09-09 19:39:16.992681 GSK (5709, 7) 1999-12-31 00:00:00 2022-09-08 00:00:00

2022-09-09 19:39:17.367706 NVO (5709, 7) 1999-12-31 00:00:00 2022-09-08 00:00:00

2022-09-09 19:39:17.680497 AROC (3790, 7) 2007-08-21 00:00:00 2022-09-08 00:00:00

2022-09-09 19:39:17.978139 GKOS (1815, 7) 2015-06-25 00:00:00 2022-09-08 00:00:00

ticker = 'GKOS'

dfs[ticker].tail(5)

| Open | High | Low | Close | Volume | Dividends | Stock Splits | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2022-09-01 | 48.209999 | 48.919998 | 46.900002 | 48.840000 | 372500 | 0 | 0 |

| 2022-09-02 | 49.590000 | 50.900002 | 48.419998 | 48.830002 | 650900 | 0 | 0 |

| 2022-09-06 | 49.200001 | 49.200001 | 47.630001 | 48.099998 | 334400 | 0 | 0 |

| 2022-09-07 | 52.759998 | 60.919998 | 51.490002 | 57.009998 | 4560500 | 0 | 0 |

| 2022-09-08 | 56.439999 | 59.599998 | 56.439999 | 58.380001 | 1106900 | 0 | 0 |

Define NVAMA calculation function

//@version=2

study("VAMA",overlay=true)

length = input(14)

//----

c = sma(close,length)

o = sma(open,length)

h = sma(high,length)

l = sma(low,length)

lv = abs(c-o)/(h - l)

//----

ma = lv*close+(1-lv)*nz(ma[1],close)

plot(ma,color=#FF0000,transp=0)

def cal_nvama(ohlc: pd.DataFrame, period: int = 14) -> pd.Series:

"""

A New Adaptive Moving Average: VAMA

:period: Specifies the number of periods used for VAMA calculation

based on: https://mpra.ub.uni-muenchen.de/94323/1/MPRA_paper_94323.pdf

"""

ohlc = ohlc.copy(deep=True)

ohlc.columns = [col_name.lower() for col_name in ohlc.columns]

c = ohlc.close.rolling(period).mean()

o = ohlc.open.rolling(period).mean()

h = ohlc.high.rolling(period).mean()

l = ohlc.low.rolling(period).mean()

lv = abs(c - o)/(h - l)

ma = lv*ohlc.close + (1 - lv)*ohlc.close.shift(1)

return pd.Series(ma, index=ohlc.index, name=f"NVAMA{period}")

Calculate NVAMA

df = dfs[ticker][['Open', 'High', 'Low', 'Close', 'Volume']]

df = df.round(2)

df_ta = cal_nvama(df, period = 14)

df = df.merge(df_ta, left_index = True, right_index = True, how='inner' )

del df_ta

gc.collect()

101

display(df.head(5))

display(df.tail(5))

| Open | High | Low | Close | Volume | NVAMA14 | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2015-06-25 | 29.11 | 31.95 | 28.00 | 31.22 | 7554700 | NaN |

| 2015-06-26 | 30.39 | 30.39 | 27.51 | 28.00 | 1116500 | NaN |

| 2015-06-29 | 27.70 | 28.48 | 27.51 | 28.00 | 386900 | NaN |

| 2015-06-30 | 27.39 | 29.89 | 27.39 | 28.98 | 223900 | NaN |

| 2015-07-01 | 28.83 | 29.00 | 27.87 | 28.00 | 150000 | NaN |

| Open | High | Low | Close | Volume | NVAMA14 | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2022-09-01 | 48.21 | 48.92 | 46.90 | 48.84 | 372500 | 48.553668 |

| 2022-09-02 | 49.59 | 50.90 | 48.42 | 48.83 | 650900 | 48.838361 |

| 2022-09-06 | 49.20 | 49.20 | 47.63 | 48.10 | 334400 | 48.667913 |

| 2022-09-07 | 52.76 | 60.92 | 51.49 | 57.01 | 4560500 | 48.147812 |

| 2022-09-08 | 56.44 | 59.60 | 56.44 | 58.38 | 1106900 | 57.072998 |

#https://github.com/matplotlib/mplfinance

#this package help visualize financial data

import mplfinance as mpf

import matplotlib.colors as mcolors

# all_colors = list(mcolors.CSS4_COLORS.keys())#"CSS Colors"

all_colors = list(mcolors.TABLEAU_COLORS.keys()) # "Tableau Palette",

# all_colors = list(mcolors.BASE_COLORS.keys()) #"Base Colors",

#https://github.com/matplotlib/mplfinance/issues/181#issuecomment-667252575

#list of colors: https://matplotlib.org/stable/gallery/color/named_colors.html

#https://github.com/matplotlib/mplfinance/blob/master/examples/styles.ipynb

def plot_3panels(main_data, add_data=None, mid_panel=None, chart_type='candle', names=None,

figratio=(14,9)):

style = mpf.make_mpf_style(base_mpf_style='yahoo', #charles

base_mpl_style = 'seaborn-whitegrid',

# marketcolors=mpf.make_marketcolors(up="r", down="#0000CC",inherit=True),

gridcolor="whitesmoke",

gridstyle="--", #or None, or - for solid

gridaxis="both",

edgecolor = 'whitesmoke',

facecolor = 'white', #background color within the graph edge

figcolor = 'white', #background color outside of the graph edge

y_on_right = False,

rc = {'legend.fontsize': 'small',#or number

#'figure.figsize': (14, 9),

'axes.labelsize': 'small',

'axes.titlesize':'small',

'xtick.labelsize':'small',#'x-small', 'small','medium','large'

'ytick.labelsize':'small'

},

)

if (chart_type is None) or (chart_type not in ['ohlc', 'line', 'candle', 'hollow_and_filled']):

chart_type = 'candle'

len_dict = {'candle':2, 'ohlc':3, 'line':1, 'hollow_and_filled':2}

kwargs = dict(type=chart_type, figratio=figratio, volume=True, volume_panel=1,

panel_ratios=(4,2), tight_layout=True, style=style, returnfig=True)

if names is None:

names = {'main_title': '', 'sub_tile': ''}

added_plots = {

'NVAMA14': mpf.make_addplot(add_data['NVAMA14'], panel=0, color='dodgerblue', secondary_y=False),

# 'AO-SIGNAL': mpf.make_addplot(mid_panel['AO']-mid_panel['SIGNAL'], type='bar',width=0.7,panel=1, color="pink",alpha=0.65,secondary_y=False),

}

fig, axes = mpf.plot(main_data, **kwargs,

addplot=list(added_plots.values()),

)

# add a new suptitle

fig.suptitle(names['main_title'], y=1.05, fontsize=12, x=0.128)

axes[0].set_title(names['sub_tile'], fontsize=10, style='italic', loc='left')

#set legend

# axes[0].legend([None]*6)

# handles = axes[0].get_legend().legendHandles

# print(handles)

# axes[0].legend(handles=handles[4:],labels=['MAMA', 'FAMA'])

#axes[2].set_title('AO', fontsize=10, style='italic', loc='left')

# axes[0].set_ylabel('MAMA')

# axes[0].set_ylabel(names['y_tiles'][0])

return fig, axes

start = -100

end = df.shape[0]

names = {'main_title': f'{ticker}',

'sub_tile': 'NVAMA: a New Adaptive Moving Average'}

aa_, bb_ = plot_3panels(df.iloc[start:end][['Open', 'High', 'Low', 'Close', 'Volume']],

df.iloc[start:end][[ 'NVAMA14']],

None,

chart_type='hollow_and_filled',

names = names,

)