Deep Adaptive Input Normalization for Time Series Forecasting

References

- Passalis, N., Kanniainen, J., Gabbouj, M. et al. Forecasting Financial Time Series Using Robust Deep Adaptive Input Normalization. J Sign Process Syst 93, 1235–1251 (2021). https://doi.org/10.1007/s11265-020-01624-0

- source code

Notes on Paper

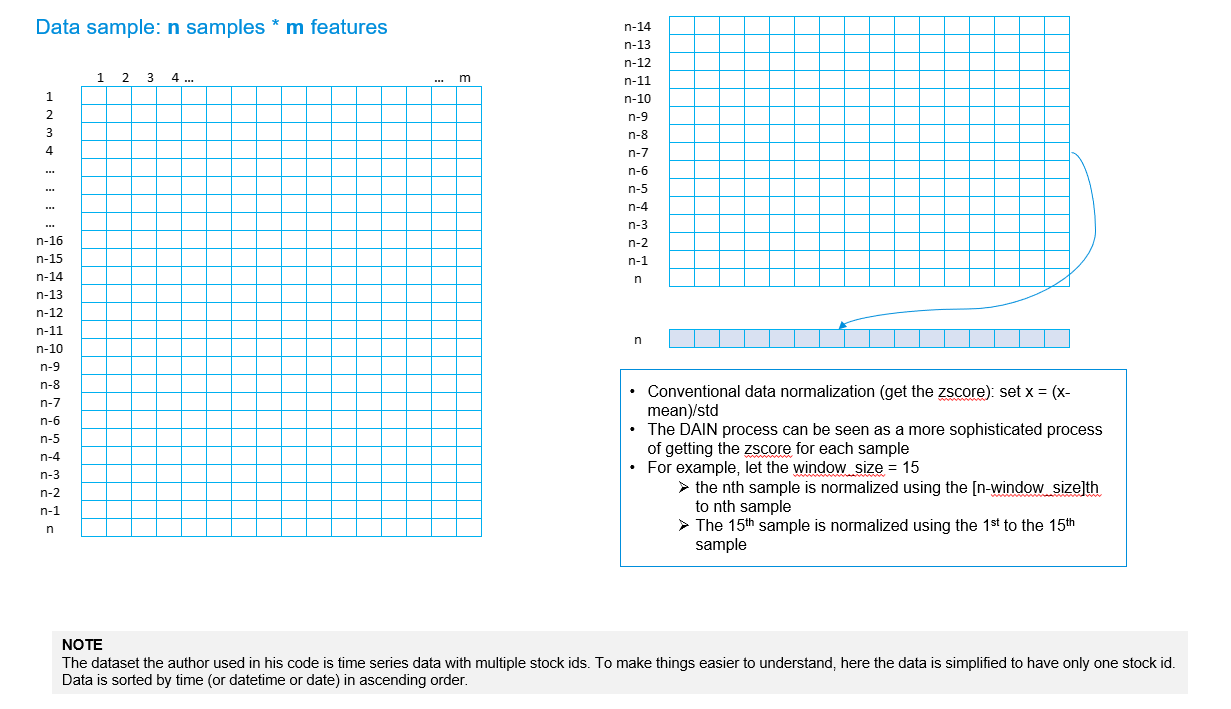

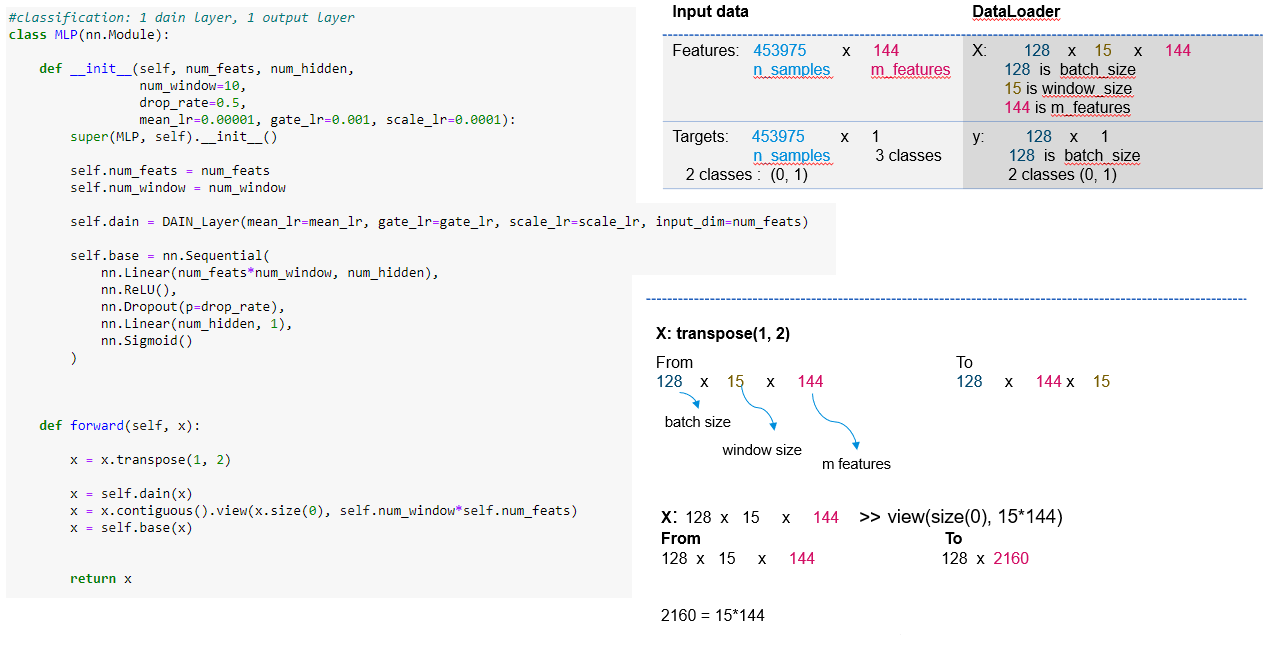

- the authors of this paper proposed a data normalization layer called deep adaptive input normalization before the neural network learning layers to normalize data that aims to address the non-stationary issue of time series data.

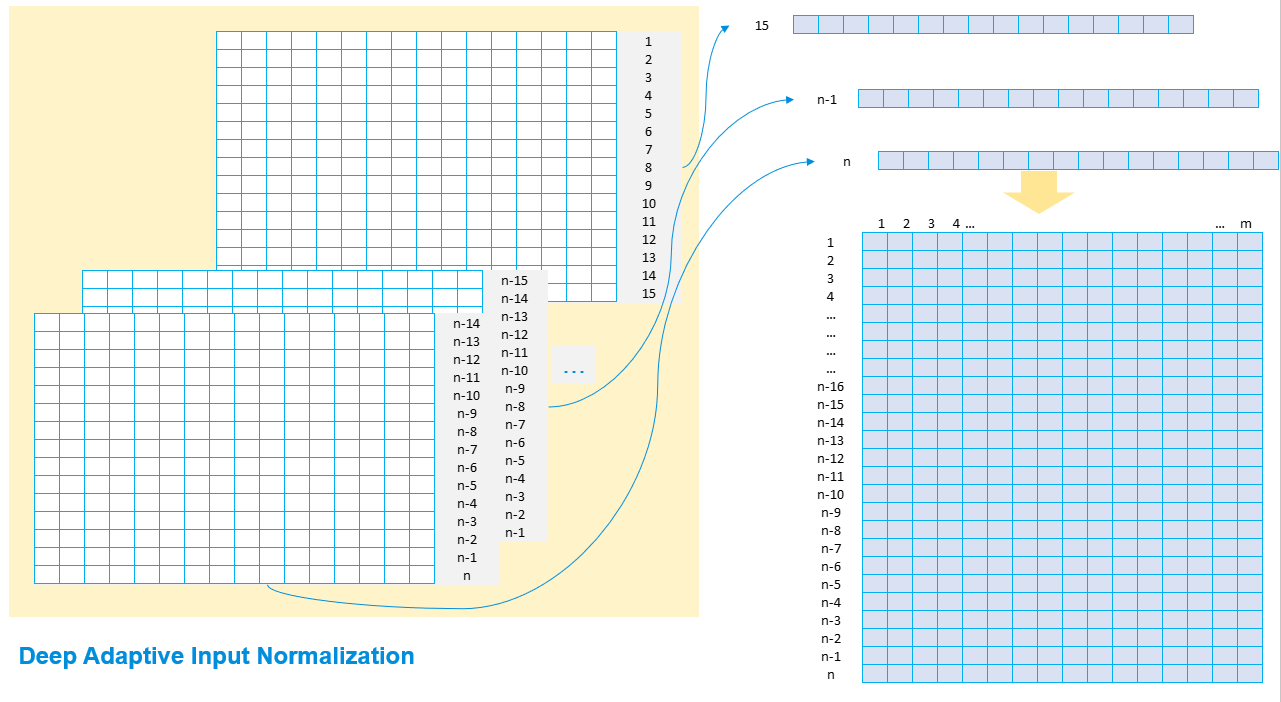

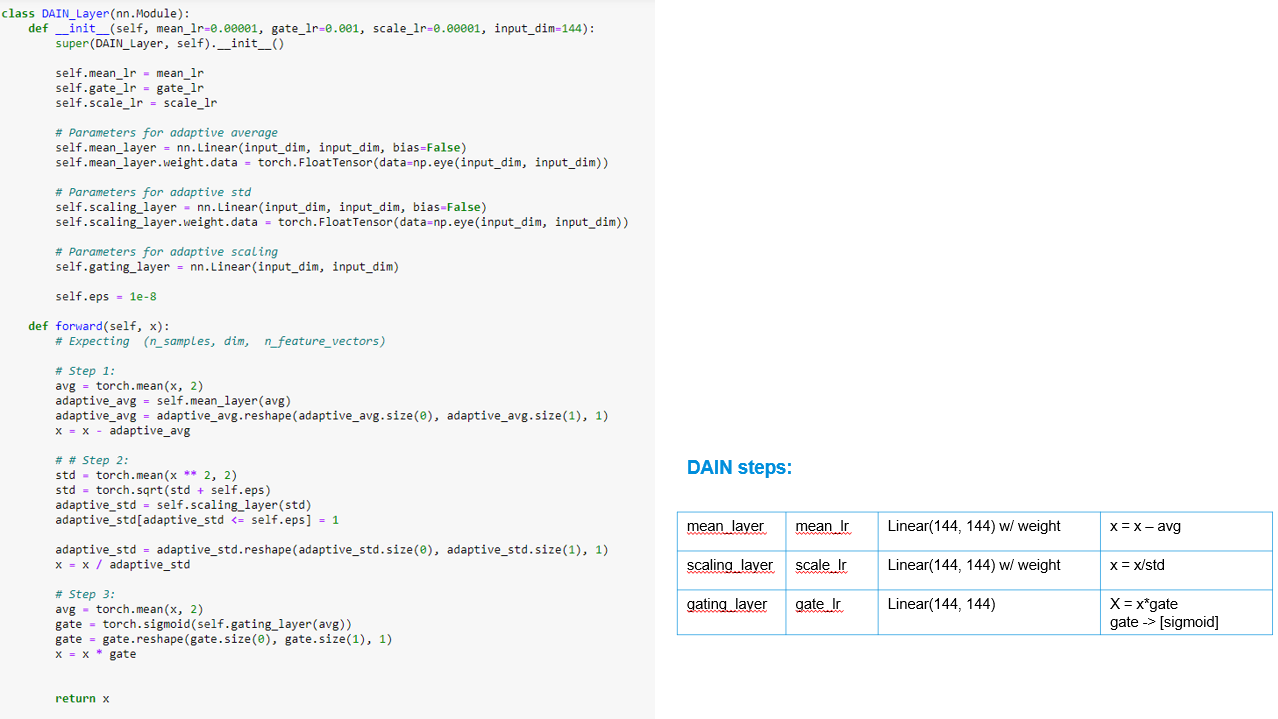

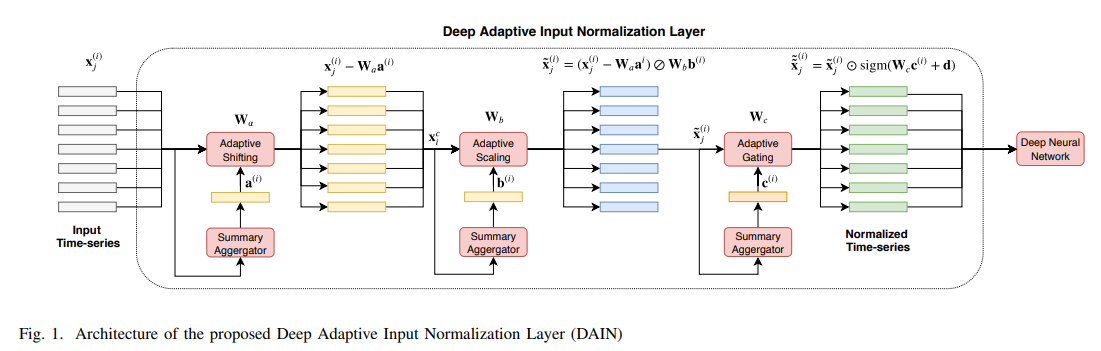

- the architecture of the normalization layer outlines 3 steps - as is shown in the following figure:

- use of mean: x = x - mean

- use of standard deviation (std): x = x/std

- use of sigmoid: x = x*sigmoid

Visual Explanation of DAIN process