Tabnet hyperparamter tuning with hyperopt - regression

reference:

- https://github.com/dreamquark-ai/tabnet/blob/develop/regression_example.ipynb

- https://arxiv.org/pdf/1908.07442.pdf

- http://hyperopt.github.io/hyperopt/

steps:

- download market data using yfinance: download S&P 500 (‘^GSPC')

- create target variable: calculate return 20-day max return (i.e. target in supervised learning problem).

- for each date (T):

- calculate the max price change in next 20 trading dates: price_change = (max{close price in T+1 to T+20} - {close price on T})/({close price on T})

- for each date (T):

- feature engineering: engineer a few features

- lag21: previous 21 day target

- lag31: previous 31 day target

- lag41: previous 41 day target

- day price change: the difference between open and closing prices

- (Close - Open)/Open

- day max price change: the difference between high and low prices

- (High-Low)/Open

- one day close price change: day T close price versus day T-1 close price.

- 100*({Close on T} - {Close on T-1})/{Close on T-1}

- 10 day close price change: day T close price versus day T-10 close price.

- 100*({Close on T} - {Close on T-10})/{Close on T-10}

- 20 day close price change: day T close price versus day T-20 close price.

- 100*({Close on T} - {Close on T-20})/{Close on T-20}

- one day/10day/20day volume change

- processing data and split data into training and testing subsets

- setup the hyperparamter search space.

- the search space is defined based on 1) hyperparamters defined on this page and the search space described in TabNet original paper

- I also added max number of epoches to search space, and I am not using any early stop (the early stop parametr in TabNet is

patience- Number of consecutive epochs without improvement before performing early stopping.

- use hyperopt to run the tuning process

- I use tpe algorithm - it is a Baysian search process with certain number of initial random trials.

- here is a full walkthrough of hyperopt pdf

- save trials and results

- dump trials into a pickle file. this file can be helpful if I later want to run more trials of hyperparamter tuning.

import numpy as np

import pandas as pd

from datetime import datetime, timedelta

import yfinance as yf #to download stock price data

from pytorch_tabnet.tab_model import TabNetClassifier

import torch

from sklearn.preprocessing import LabelEncoder

from sklearn.metrics import accuracy_score

import pandas as pd

import numpy as np

import os

from pathlib import Path

import shutil

#initiate random seed

rand_seed=568

import random

def init_seed(random_seed):

random.seed(random_seed)

os.environ['PYTHONHASHSEED'] = str(random_seed)

np.random.seed(random_seed)

torch.manual_seed(random_seed)

if torch.cuda.is_available():

torch.cuda.manual_seed(random_seed)

torch.cuda.manual_seed_all(random_seed)

torch.backends.cudnn.deterministic = True

torch.backends.cudnn.benchmark = False

init_seed(rand_seed)

import plotly.express as px

import plotly.graph_objects as go

from plotly.subplots import make_subplots

download S&P 500 price data

ticker = '^GSPC'

cur_data = yf.Ticker(ticker)

hist = cur_data.history(period="max")

print(ticker, hist.shape, hist.index.min())

^GSPC (19721, 7) 1927-12-30 00:00:00

df=hist[hist.index>='2000-01-01'].copy(deep=True)

df.head()

| Open | High | Low | Close | Volume | Dividends | Stock Splits | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2000-01-03 | 1469.250000 | 1478.000000 | 1438.359985 | 1455.219971 | 931800000 | 0 | 0 |

| 2000-01-04 | 1455.219971 | 1455.219971 | 1397.430054 | 1399.420044 | 1009000000 | 0 | 0 |

| 2000-01-05 | 1399.420044 | 1413.270020 | 1377.680054 | 1402.109985 | 1085500000 | 0 | 0 |

| 2000-01-06 | 1402.109985 | 1411.900024 | 1392.099976 | 1403.449951 | 1092300000 | 0 | 0 |

| 2000-01-07 | 1403.449951 | 1441.469971 | 1400.729980 | 1441.469971 | 1225200000 | 0 | 0 |

create the target variable: calcualte max return in next 20 trading days

#for each stock_id, get the max close in next 20 trading days

price_col = 'Close'

roll_len=20

new_col = 'next_20day_max'

target_list = []

df.sort_index(ascending=True, inplace=True)

df.head(3)

| Open | High | Low | Close | Volume | Dividends | Stock Splits | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2000-01-03 | 1469.250000 | 1478.000000 | 1438.359985 | 1455.219971 | 931800000 | 0 | 0 |

| 2000-01-04 | 1455.219971 | 1455.219971 | 1397.430054 | 1399.420044 | 1009000000 | 0 | 0 |

| 2000-01-05 | 1399.420044 | 1413.270020 | 1377.680054 | 1402.109985 | 1085500000 | 0 | 0 |

df_next20dmax=df[[price_col]].shift(1).rolling(roll_len).max()

df_next20dmax.columns=[new_col]

df = df.merge(df_next20dmax, right_index=True, left_index=True, how='inner')

df.dropna(how='any', inplace=True)

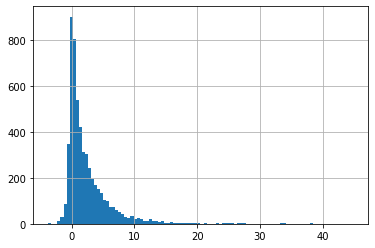

df['target']= 100*(df[new_col]-df[price_col])/df[price_col]

df['target'].describe()

count 5479.000000

mean 2.450897

std 4.077561

min -3.743456

25% 0.135604

50% 1.130147

75% 3.318523

max 44.809803

Name: target, dtype: float64

df['target'].hist(bins=100)

<AxesSubplot:>

engineer features

- lag21: previous 21 day target

- lag31: previous 31 day target

- lag41: previous 41 day target

- day price change: the difference between open and closing prices

- (Close - Open)/Open

- day max price change: the difference between high and low prices

- (High-Low)/Open

- one day close price change: day T close price versus day T-1 close price.

- 100*({Close on T} - {Close on T-1})/{Close on T-1}

- 10 day close price change: day T close price versus day T-10 close price.

- 100*({Close on T} - {Close on T-10})/{Close on T-10}

- 20 day close price change: day T close price versus day T-20 close price.

- 100*({Close on T} - {Close on T-20})/{Close on T-20}

- one day/10day/20day volume change

df['lag21']=df['target'].shift(21)

df['lag31']=df['target'].shift(31)

df['lag41']=df['target'].shift(41)

df['open_close_diff'] = df['Close'] - df['Open']

df['day_change']=(100*df['open_close_diff']/df['Open']).round(2)

df['day_max_change'] = (100*(df['High'] - df['Low'])/df['Open']).round(2)

#create a binary feature: 1 day change

#0: decrease; 1: increase

df['oneday_change']=(df['Close'].diff()>0)+1-1

df['10day_change']=df['Close'].diff(10)

df['20day_change']=df['Close'].diff(20)

df['oneday_volchange']=(df['Volume'].diff()>0)+1-1

df['10day_volchange']=df['Volume'].diff(10)

df['20day_volchange']=df['Volume'].diff(20)

df.head(3)

| Open | High | Low | Close | Volume | Dividends | Stock Splits | next_20day_max | target | lag21 | ... | lag41 | open_close_diff | day_change | day_max_change | oneday_change | 10day_change | 20day_change | oneday_volchange | 10day_volchange | 20day_volchange | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2000-02-01 | 1394.459961 | 1412.489990 | 1384.790039 | 1409.280029 | 981000000 | 0 | 0 | 1465.150024 | 3.964435 | NaN | ... | NaN | 14.820068 | 1.06 | 1.99 | 0 | NaN | NaN | 0 | NaN | NaN |

| 2000-02-02 | 1409.280029 | 1420.609985 | 1403.489990 | 1409.119995 | 1038600000 | 0 | 0 | 1465.150024 | 3.976243 | NaN | ... | NaN | -0.160034 | -0.01 | 1.21 | 0 | NaN | NaN | 1 | NaN | NaN |

| 2000-02-03 | 1409.119995 | 1425.780029 | 1398.520020 | 1424.969971 | 1146500000 | 0 | 0 | 1465.150024 | 2.819712 | NaN | ... | NaN | 15.849976 | 1.12 | 1.93 | 1 | NaN | NaN | 1 | NaN | NaN |

3 rows × 21 columns

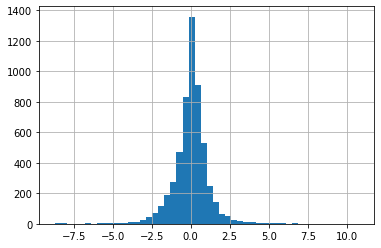

df['day_change'].hist(bins=50)

<AxesSubplot:>

#convert day_change into categorical feature

#above 2- class 1; below -2 - class -1, in the middle - class0

df['day_change_cat']=0

df.loc[df['day_change']<=-2, 'day_change_cat']=-1

df.loc[df['day_change']>=2, 'day_change_cat']=1

df['day_change_cat'].value_counts()

0 5095

-1 210

1 174

Name: day_change_cat, dtype: int64

df.dropna(how='any', inplace=True)

print(df.shape, df.index.min())

df.head(3)

(5438, 22) 2000-03-30 00:00:00

| Open | High | Low | Close | Volume | Dividends | Stock Splits | next_20day_max | target | lag21 | ... | open_close_diff | day_change | day_max_change | oneday_change | 10day_change | 20day_change | oneday_volchange | 10day_volchange | 20day_volchange | day_change_cat | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2000-03-30 | 1508.520020 | 1517.380005 | 1474.630005 | 1487.920044 | 1193400000 | 0 | 0 | 1527.459961 | 2.657395 | 4.533823 | ... | -20.599976 | -1.37 | 2.83 | 0 | 29.450073 | 106.160034 | 1 | -288900000.0 | -5200000.0 | 0 |

| 2000-03-31 | 1487.920044 | 1519.810059 | 1484.380005 | 1498.579956 | 1227400000 | 0 | 0 | 1527.459961 | 1.927158 | 4.339390 | ... | 10.659912 | 0.72 | 2.38 | 1 | 34.109985 | 89.409912 | 1 | -67700000.0 | 77100000.0 | 0 |

| 2000-04-03 | 1498.579956 | 1507.189941 | 1486.959961 | 1505.969971 | 1021700000 | 0 | 0 | 1527.459961 | 1.426987 | 2.309865 | ... | 7.390015 | 0.49 | 1.35 | 1 | 49.339966 | 114.689941 | 0 | 100900000.0 | -7300000.0 | 0 |

3 rows × 22 columns

categorical data processing for TabNet

target='target'

df.dropna(how='any', inplace=True)

train = df.copy(deep=True)

categorical_columns = ['day_change_cat']

categorical_dims = {}

for col in categorical_columns:

print(col, train[col].nunique())

l_enc = LabelEncoder()

train[col] = l_enc.fit_transform(train[col].values)

categorical_dims[col] = len(l_enc.classes_)

categorical_dims

day_change_cat 3

{'day_change_cat': 3}

categorical_columns, categorical_dims

(['day_change_cat'], {'day_change_cat': 3})

Define categorical features for categorical embeddings

unused_feat = ['Dividends', 'Stock Splits', 'next_20day_max',

'open_close_diff', 'day_change' ]

features = [ col for col in train.columns if col not in unused_feat+[target]]

cat_idxs = [ i for i, f in enumerate(features) if f in categorical_columns]

cat_dims = [ categorical_dims[f] for i, f in enumerate(features) if f in categorical_columns]

print(features, len(features))

['Open', 'High', 'Low', 'Close', 'Volume', 'lag21', 'lag31', 'lag41', 'day_max_change', 'oneday_change', '10day_change', '20day_change', 'oneday_volchange', '10day_volchange', '20day_volchange', 'day_change_cat'] 16

cat_idxs

[15]

cat_dims

[3]

Split data from training

train.shape

(5438, 22)

X_train = train[features].values[:-1000,:]

y_train = train[target].values[:-1000]

X_test = train[features].values[-950:, ]

y_test = train[target].values[-950:]

X_train.shape, X_test.shape

((4438, 16), (950, 16))

hyperopt setup - define search space and score function

from hyperopt import hp

from hyperopt import fmin, tpe, hp, STATUS_OK, Trials, anneal, rand

search_space = {

'n_d': hp.choice('n_d',[8, 16, 24, 32, 64, 128]), #Nd and Na are chosen from {8, 16, 24, 32, 64, 128},

'n_steps': hp.choice('n_steps',[3,4,5,6,7,8,9,10]),#Nsteps is chosen from {3, 4, 5, 6, 7, 8, 9, 10}

'gamma':hp.choice('gamma', [1.0, 1.2, 1.5, 2.0]),#γ is chosen from {1.0, 1.2, 1.5, 2.0}

'n_independent':hp.choice('n_independent', [1,2,3,4,5] ),

'n_shared':hp.choice('n_shared', [1,2,3,4,5]),

'momentum': hp.choice('momentum', np.round(np.arange(0.01, 0.4, 0.01),3)), #Momentum for batch normalization, typically ranges from 0.01 to 0.4 (default=0.02)

#momentum mB., and mB is chosen from {0.6, 0.7, 0.8, 0.9, 0.95, 0.98}.

'lambda_sparse': hp.choice('lambda_sparse', [0, 0.000001, 0.0001, 0.001, 0.01, 0.1]), #λsparse is chosen from {0, 0.000001, 0.0001, 0.001, 0.01, 0.1}

'optimizer_fn': hp.choice('optimizer_fn', ['Adam', 'RMSprop', 'SGD']),

'lr': hp.choice('lr', [0.005, 0.01, 0.02, 0.025]), #optimizer. the learning rateis chosen from {0.005, 0.01.0.02, 0.025},

'optimizer_momentum': hp.choice('optimizer_momentum', [0.4, 0.8, 0.9, 0.95]),#optimizer ????

#the decay rate is chosen from {0.4, 0.8, 0.9, 0.95} and the decay iterations is chosen from {0.5k, 2k, 8k, 10k, 20k}

'weight_decay':hp.choice('weight_decay', [0, 0.5, 0.001, 0.0001] ),#optimizer. the decay rate is chosen from {0.4, 0.8, 0.9, 0.95} a

'scheduler_fn':hp.choice('scheduler_fn', ['StepLR', 'CosineAnnealingWarmRestarts', 'ReduceLROnPlateau']),

'fn_step_size':hp.choice('fn_step_size', [3, 5, 10, 15]),

'fn_gamma':hp.choice('fn_gamma', np.round(np.arange(0.1, 0.95, 0.01),3)),

'fn_T_0':hp.choice('fn_T_0', [3, 5, 10, 15]),

'fn_eta_min':hp.choice('fn_eta_min', np.round(np.arange(0.0001, 0.001, 0.0001),4)),

'max_epochs':hp.choice('max_epochs', range(30, 201, 1)),

'batch_size':hp.choice('batch_size', [256, 512, 1024, 2048, 4096, 8192, 16384, 32768]),#B is chosen from {256, 512, 1024, 2048, 4096, 8192, 16384, 32768}

'virtual_batch_size':hp.choice('virtual_batch_size', [256, 512, 1024, 2048, 4096]),#BV is chosen from {256, 512, 1024, 2048, 4096}

'patience':hp.choice('patience', [0]),

}

n_trials = 100

n_random_trials = 30

from pytorch_tabnet.tab_model import TabNetRegressor

import torch

from sklearn.preprocessing import LabelEncoder

from sklearn.preprocessing import label_binarize

from sklearn.metrics import mean_squared_error

import copy

def score(params):

tab_params = {}

tab_params['n_d'] = params['n_d']

tab_params['n_a'] = params['n_d'] #set n_a equals n_d according to official document

tab_params['seed']= rand_seed #set random seed for reproduciablity

tab_params['gamma'] = params['gamma']

tab_params['n_independent'] = params['n_independent']

tab_params['n_shared'] = params['n_shared']

tab_params['momentum'] = params['momentum']

tab_params['lambda_sparse'] = params['lambda_sparse']

tab_params['cat_idxs']=cat_idxs #no categorical features

tab_params['cat_dims']=cat_dims

tab_params['cat_emb_dim']=1,

lr =params['lr']

weight_decay =params['weight_decay']

optimizer_momentum =params['optimizer_momentum']

optimizer_fn=params['optimizer_fn']

if optimizer_fn=='Adam':

tab_params['optimizer_params'] = dict(lr=lr, weight_decay=weight_decay)

tab_params['optimizer_fn'] = torch.optim.Adam

elif optimizer_fn == 'RMSprop':

tab_params['optimizer_params'] = dict(lr=lr, momentum=optimizer_momentum, weight_decay=weight_decay)

tab_params['optimizer_fn'] = torch.optim.RMSprop

elif optimizer_fn == 'SGD':

tab_params['optimizer_params'] = dict(lr=lr, momentum=optimizer_momentum, weight_decay=weight_decay)

tab_params['optimizer_fn'] = torch.optim.SGD

scheduler_fn = params['scheduler_fn']

fn_step_size = params['fn_step_size']

fn_gamma = params['fn_gamma']

fn_T_0 = params['fn_T_0']

fn_eta_min = params['fn_eta_min']

if scheduler_fn== 'StepLR':

tab_params['scheduler_params'] ={'gamma':fn_gamma, 'step_size':fn_step_size}

tab_params['scheduler_fn'] = torch.optim.lr_scheduler.StepLR

elif scheduler_fn== 'CosineAnnealingWarmRestarts':

tab_params['scheduler_params'] ={'T_0':fn_T_0, 'eta_min':fn_eta_min}

tab_params['scheduler_fn'] = torch.optim.lr_scheduler.CosineAnnealingWarmRestarts

elif scheduler_fn== 'ReduceLROnPlateau':

tab_params['scheduler_params'] ={'mode':'min', 'min_lr':fn_eta_min}

tab_params['scheduler_fn'] = torch.optim.lr_scheduler.ReduceLROnPlateau

tab_params['epsilon']=1e-15 #default. leave untouched

tab_params['verbose']=0 #no verbose

batch_size=params['batch_size']

mini_batch_size=params['virtual_batch_size']

if mini_batch_size>batch_size:

mini_batch_size=batch_size

#--add fit params---

full_params = copy.deepcopy(tab_params)

max_epochs = params['max_epochs']

patience = params['patience']

full_params['max_epochs'] = max_epochs

full_params['batch_size'] = batch_size

full_params['virtual_batch_size'] = mini_batch_size

full_params['patience'] = patience

params_list.append(copy.deepcopy(full_params))

#-----------------------------------------------------

#---start training: this part can easily be replaced with k-fold list----

i = len(params_list)

#initiate classifier - need to re-initiate for each Train-Test pair

clf = TabNetRegressor(**tab_params)

clf.fit(

X_train=X_train, y_train=y_train.reshape(-1,1),

eval_set=[(X_train, y_train.reshape(-1,1))],

eval_name=['train'],

eval_metric=['mse'],

max_epochs=max_epochs, patience=patience,

batch_size=batch_size, virtual_batch_size=mini_batch_size,

num_workers=0,

drop_last=False

)

preds = clf.predict(X_test).flatten()

#print(preds)

loss = mean_squared_error(y_pred=preds, y_true=y_test)

df_pred = pd.DataFrame({'y_true':y_test, 'y_pred':preds})

metric_list.append([i, full_params, loss] )

df_pred.to_csv(save_dir.joinpath(f'trial_{i}'), sep='|', index=False, compression='bz2')

return {'loss': loss, 'status': STATUS_OK}

from functools import partial

def optimize(space, evals, cores, trials, optimizer=tpe.suggest, random_state=1234, n_startup_jobs=50):

space['seed']= random_state

algo = partial(optimizer, n_startup_jobs=n_startup_jobs)

best = fmin(score, space, algo=algo, max_evals=evals, trials = trials)

return best

run hyperparamter tuning

params_list = []

metric_list = []

trials = Trials()

save_dir=Path('hyper_tune/tabnet')

optimize(search_space,

evals = 10,

optimizer=tpe.suggest,

cores = 4,

trials = trials, random_state=rand_seed,

n_startup_jobs=5)

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

No early stopping will be performed, last training weights will be used.

100%|███████████████████████████████████████████████| 10/10 [25:39<00:00, 153.91s/trial, best loss: 11.542633152981768]

{'batch_size': 6,

'fn_T_0': 0,

'fn_eta_min': 7,

'fn_gamma': 5,

'fn_step_size': 0,

'gamma': 3,

'lambda_sparse': 0,

'lr': 1,

'max_epochs': 30,

'momentum': 38,

'n_d': 1,

'n_independent': 1,

'n_shared': 3,

'n_steps': 4,

'optimizer_fn': 1,

'optimizer_momentum': 0,

'patience': 0,

'scheduler_fn': 2,

'virtual_batch_size': 3,

'weight_decay': 1}

save trials and results

- dump trials into a pickle file. this file can be helpful if I later want to run more trials of hyperparamter tuning.

save_dir.parent

WindowsPath('hyper_tune')

import joblib

joblib.dump(trials, save_dir.parent.joinpath('tabnet.pkl'))

['hyper_tune\\tabnet.pkl']

pd.DataFrame(metric_list, columns=['trial_id', 'params', 'loss']).to_excel(save_dir.parent.joinpath('tabnet.xlsx'))